The fresh housing metrics for June show that while total transaction volume is holding a steady line, buyers are finally getting a bit more real estate supply to look at.

According to the National Association of Realtors (NAR), existing home sales hit 390,000 in May. That matches last year’s figures exactly, but it shows a strong monthly gain of +9.6% from April’s adjusted numbers. On the supply side, active inventory jumped up +3.3% month-over-month to 1.55 million units. Zillow also tracked a +1% annual increase in active listings, marking two and a half straight years of year-over-year gains.

Regionally, price changes tell a divided story. The national median existing home price grew +1.3% to $429,300, according to NAR. The Northeast led the charge at $534,900 (+4.2% YoY), followed by the Midwest at $336,300 (+2.8%), and the South at $373,100 (+1.1%). Meanwhile, the West saw home prices soften slightly, dipping -0.7% to $625,900.

Borrowing costs are maintaining their current range, with Fannie Mae and the Mortgage Bankers Association projecting 30-year fixed rates in the mid-6% area through 2026 and 2027.

Current Forecasts

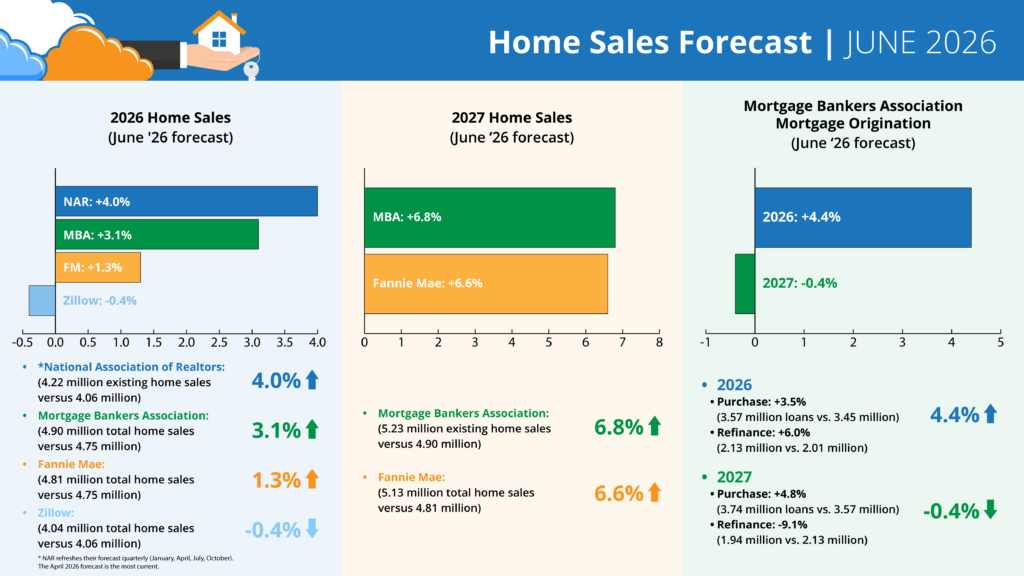

Forecasts for 2026 Home Sales (June ’26 forecast)

- NAR: +4.0% (4.22 million existing home sales vs. 4.06 million) – revised April 2026

- MBA: +3.1% (4.90 million total home sales vs. 4.75 million)

- Fannie Mae: +1.3% (4.81 million total home sales vs. 4.75 million)

- Zillow: -0.4% (4.04 million existing home sales vs. 4.06 million)

Forecasts for 2027 Home Sales (June ’26 forecast)

- MBA: +6.8% (5.23 million total home sales vs. 4.90 million)

- Fannie Mae: +6.6% (5.13 million total home sales vs. 4.81 million)

MBA Forecast for Mortgage Originations (June ’26 forecast)

- 2026 Total Mortgage Originations: +4.4% (5.70 million loans vs. 5.46 million)

- Purchase: +3.5% (3.57 million loans vs. 3.45 million)

- Refi: +6.0% (2.13 million vs. 2.01 million)

- 2027 Total Mortgage Originations: -0.4% (5.67 million loans vs. 5.70 million)

- Purchase: +4.8% (3.74 million loans vs. 3.57 million)

- Refi: -9.1% (1.94 million vs. 2.13 million)

The takeaway

Inventory is making steady headway, and sales are showing healthy month-over-month traction. That’s solid news for inspectors waiting for more transaction action. Since interest rates are expected to remain steady in the mid-6% zone, the market may not turn upside down overnight. Keep a close eye on your local inventory numbers, stay ready to deliver fast report turnarounds, and make sure your on-site systems are built to keep pace when buyers decide to pull the trigger.