If you’ve been waiting for the market to give you a little more breathing room, February’s data is a good start. While the National Association of Realtors (NAR) reports that total sales are still hovering near recent lows, we’re seeing more homes hit the market.

Zillow reports active inventory at 1.12 million units – that’s a +5% increase over last year. For inspectors, more inventory can mean more steady work. Total sales for February, according to the NAR were 257,000, a healthy +12.7% increase over January.

Regionally, NAR finds things are a bit split. The Northeast saw prices climb +3.3%, while the West saw a dip of -1.9%. Regardless of where you’re working, the long-term outlook appears stable.

Borrowing costs are also stabilizing. Both Fannie Mae and the Mortgage Bankers Association (MBA) have revised their outlooks slightly downward for 30-year mortgage rates. Fannie Mae now expects rates to hover near 6% through early 2026 before declining gradually toward the high-5% range through 2027, while MBA forecasts the 30-year fixed rate to stabilize in the 6%–6.3% range through 2027.

Current Forecasts

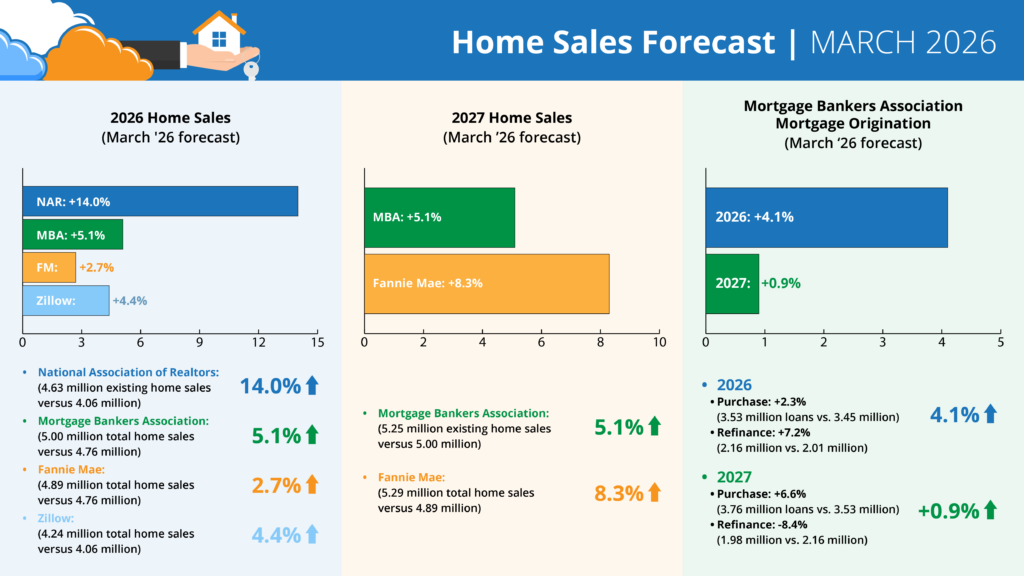

Forecasts for 2026 Home Sales (March ’26 forecast)

- NAR: +14.0% (4.63 million existing home sales vs. 4.06 million)

- MBA: +5.1% (5 million total home sales vs. 4.76 million)

- Fannie: +2.7% (4.89 million total home sales vs. 4.76 million)

- Zillow: +4.4% (4.24 million existing home sales vs. 4.06 million)

Forecasts for 2027 Home Sales (March ’26 forecast)

- MBA: +5.1% (5.25 million total home sales vs. 5 million)

- Fannie: +8.3% (5.29 million total home sales vs. 4.89 million)

MBA Forecast for Mortgage Originations (March ’26 forecast)

- 2026 Total Mortgage Originations: +4.1% (5.68 million loans vs. 5.46 million)

- Purchase: +2.3% (3.53 million loans vs. 3.45 million)

- Refi: +7.2% (2.16 million vs. 2.01 million)

2027 Total Mortgage Originations:

- +0.9% (5.73 million loans vs. 5.68 million)

- Purchase: +6.6% (3.76 million loans vs. 3.53 million)

- Refi: -8.4% (1.98 million vs. 2.16 million)

The takeaway

This month shows a market that is split but stabilizing. While the West saw a dip of -1.9% in prices, the Northeast climbed +3.3%, showing that real estate is still a local game. With more inventory on the horizon and borrowing costs trending downward, there’s potential opportunity for inspectors who are ready to hustle. Keep an eye on those active listings – they’re the best indicator for your next booking.